How to Build a Paper Trading System to Test Your Strategy

Learn how to build a paper trading system to test your algo-trading strategy effectively.

Learn how to build a paper trading system to test your algo-trading strategy effectively.

Learn about the Coinbase Advanced Trade API and how to use it for algorithmic trading in this comprehensive guide.

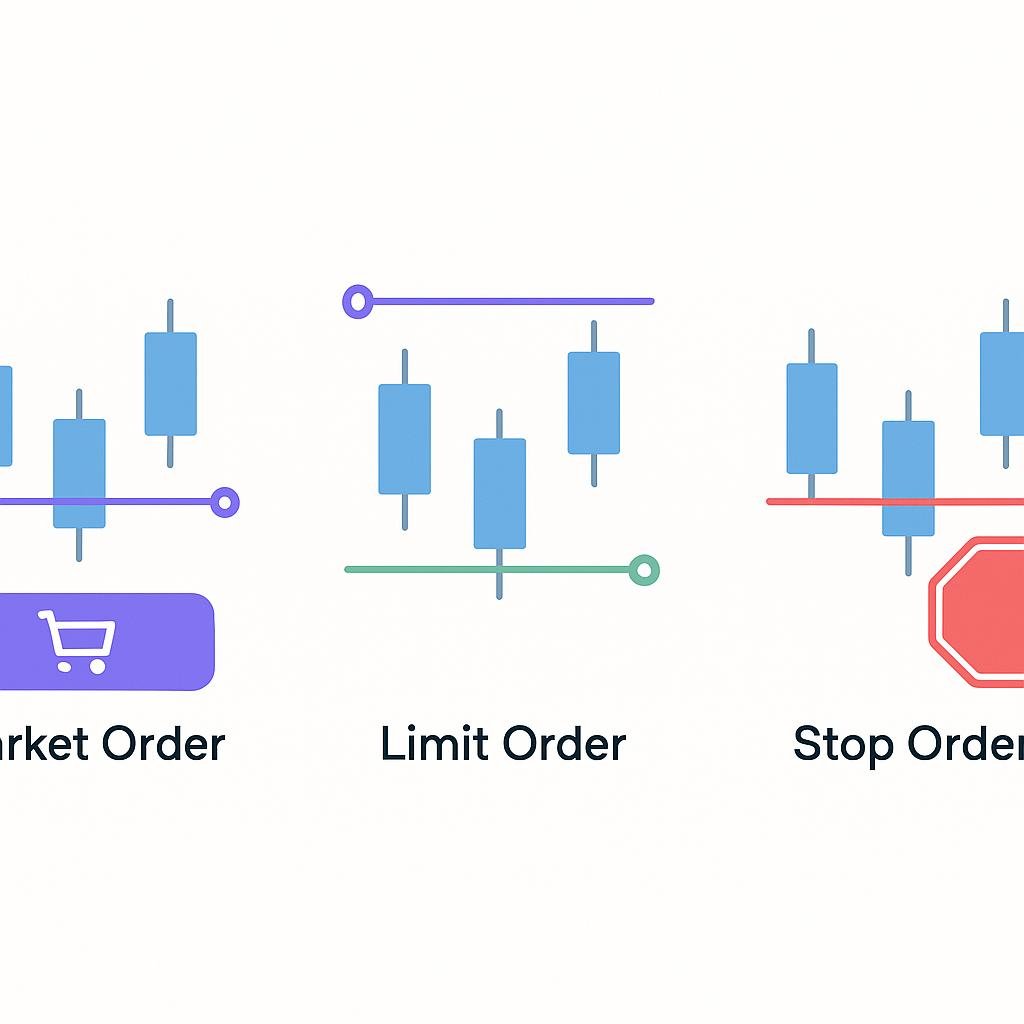

Understand market, limit, and stop orders in algo-trading with our detailed guide.

Learn how to build your first trading bot in Python with this step-by-step guide. Perfect for beginners in algo-trading.

Learn effective backtesting techniques to evaluate trading strategies accurately and avoid common pitfalls in algo-trading.

Explore algorithmic trading: how it works, its benefits, and who uses it in the financial markets for efficient and automated trading.

Explore the effectiveness of the Moving Average Crossover Strategy in algo-trading with insights and analysis.

Learn about the Kelly Criterion and its application in algo-trading for optimal bet sizing and risk management.

Explore market microstructure essentials and their importance for algorithmic traders in optimizing trading strategies.

Explore comprehensive risk management strategies for algorithmic traders in this complete guide. Essential insights for smarter trading.